As a Chelsea fan I was delighted with the outcome of last weekend’s FA Cup semi-final between Chelsea and Manchester City. But Chelsea’s defensive solidity and delightful counter attacking play is not what this article is about. The game provided a more useful output for me in that it reinforced the importance of being able to correctly assess probabilities when making and judging other people’s assumptions. So even if you are not a fan of football, stick with me because this has a direct impact on investing.

In the build up to the FA Cup semi-final there was A LOT of talk about Man City’s chances of winning the quadruple (the Premier League, FA Cup, League Cup and Champions League). It had got to the point where many pundits were saying that it was “likely” and the betting odds got down to as low as 7/2 last week. This is an implied probability of 22%. This is not the fault of the betting companies but a reflection on what people were willing to pay to make the bet that Manchester City would win the quadruple.

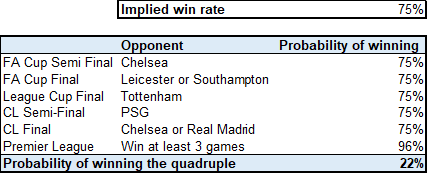

Manchester City are an exceptional team and the odds of them winning any individual game of football are high at the moment, but this seemed too generous to the bookmakers. So, taking the implied 22% chance of Manchester City winning the quadruple, I decided to work out what this implied their chances of winning each game was.

I have simplified Man City’s route to the quadruple for the sake of estimating the probabilities (see footnotes for more details on this). But my main inputs are 1) They had to win all 5 of their knockout fixtures (to win the League Cup, FA Cup and Champions League), 2) win at least 3 of their remaining Premier League fixtures to secure the title, 3) Manchester City’s chances of winning each game are the same (the assumption I am least happy with).

The implied win rate I backed out of this (simplistic) model was 75%. Not only is this higher than their achieved win rate in the Premier League this season but it also doesn’t take into account that the quality of their opponents in this string of games is much higher than the average opponent they have faced this season. As it turned out, they fell at the first hurdle against a Chelsea side reinvigorated under Thomas Tuchel’s stewardship. With the benefit of hindsight, I would say that cognitive errors in people’s thinking meant people incorrectly extrapolated Manchester City’s odds of winning an individual game into their odds of winning the quadruple, an easy behavioural trap to fall into.

So, why is this relevant? Just like sports betting odds, equity prices are made up of expectations and they can become mispriced from time to time. Exuberance around an undoubtedly excellent Manchester City team led to the price of the quadruple bet being bid up to levels which implied a win rate which was probably too high. It is important to have an appreciation of the price implied expectations for individual stocks (and the wider stock market) to know when the risk/reward is in your favour or not.

I have assumed the CL Semi Final is one game rather than a two-legged encounter – two legs makes Manchester City’s chances of winning slightly higher if you assume they are the better team. I assume that Manchester City’s chances of winning each game is the same – obviously, this will vary.

For Professional Clients/ Qualified Investors only – not for Retail use or distribution.

This is a marketing communication and as such the views contained herein are not to be taken as advice or a recommendation to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are, unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and investors may not get back the full amount invested. Past performance and yield are not a reliable indicator of current and future results. There is no guarantee that any forecast made will come to pass. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. This communication is issued in Europe (excluding UK) by JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, R.C.S. Luxembourg B27900, corporate capital EUR 10.000.000. This communication is issued in the UK by JPMorgan Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. Registered in England No. 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.

0903c02a82b18a67